Homeownership as an Investment

“Renting can make sense as a lifestyle choice or because of income

constraints. As a means to building wealth, however, there is no

practical substitute for homeownership.”

“Homeownership and Wealth Creation,” editorial in The New York Times*

Typically, the purchase of a home is one of the largest financial transactions of one’s life. Owning a home has many aspects beyond the financial: Security, control, independence, pride of ownership, the ability to make changes and improvements according to your own tastes and needs. But it is also a financial investment, and has often been a very good or even spectacular one, especially over the longer term. Following are 7 of the reasons:

- Long-term economic, demographic and home-price appreciation trends:

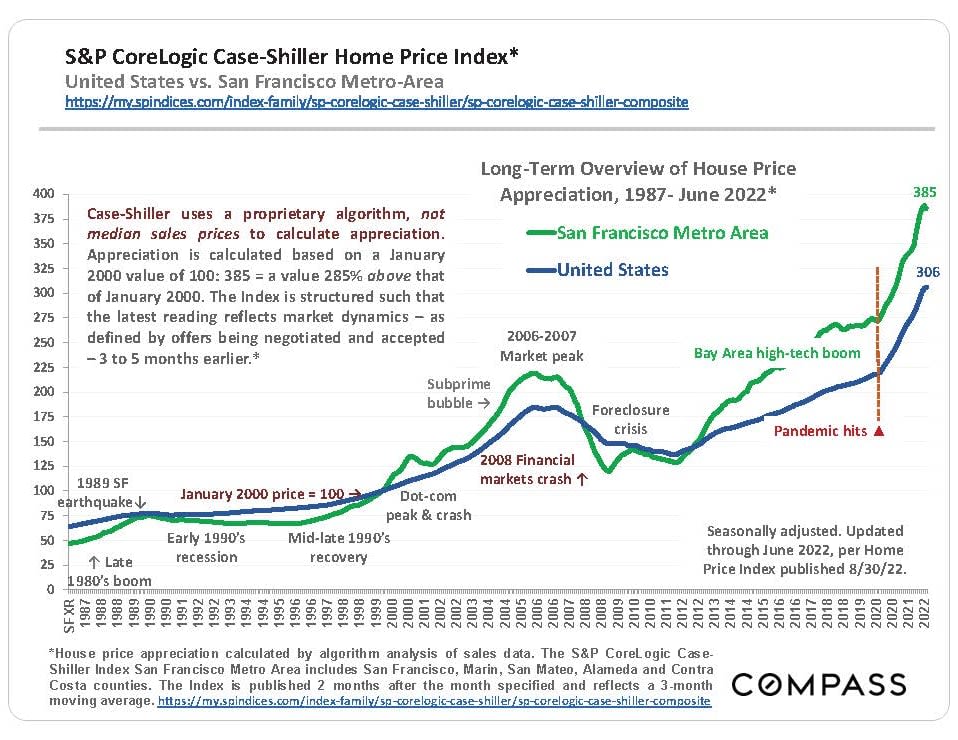

January 1990 – December 2021, the national house price appreciated 264% according to the S&P CoreLogic Case-Shiller Home Price Index, vs. a consumer-price inflation rate of approximately 120%. (The San Francisco Metro Area house-price appreciation rate was 375% over the same period.) **

- Leverage: The option to finance much of the purchase price can supercharge the return on one’s cash down-payment and closing costs if values increase.

- The ability to lock in your mortgage payment: With a fixed-rate mortgage, a major portion of one’s housing costs remains stable for the entire period of the loan, while rents typically increase significantly with inflation (or rates higher than inflation). As the years or decades pass, this can add very substantially to the financial benefit of owning vs. renting.

- The “forced savings” effect: Beside potential appreciation gains, paying one’s monthly mortgage increases home equity as the outstanding loan is gradually paid down, an effect that accelerates over the life of the loan. While rents are basically money spent and gone, mortgage payments can quietly turn into very large, equity-based, financial assets.

- The tax deductibility of certain costs of homeownership

- The $250,000/$500,000 exclusion on home-appreciation capital gains taxation

- The option of turning your home into a rental property

The home you purchase should work for you now – at minimum, fulfilling your basic housing requirements at an affordable monthly cost. (A major factor in the post-2008 crisis was tens of millions of households buying or refinancing homes with loans they couldn’t afford after so-called “teaser” rates expired.)

Keep a reserve fund in case of the unexpected developments that can come up in life.

Some other thoughts for consideration:

- Buying for the longer term is generally safer as an investment: Though it can be profitable, buying and selling over shorter periods often carries greater risks and amortized costs.

- Refinance your existing mortgage into new, long-term, fixed-rate loans when significantly lower rates make this sensible per your expected timeline of ownership. (This can be an enormous financial advantage.)

- Avoid using your home as an ATM in times of appreciation, especially for non-essentials: If possible, let your home equity grow over time, like an untouchable savings or retirement account.

Perhaps more than any other decision, buying a home combines deeply personal, quality of life issues and substantial financial considerations—which only you can weigh according to your own circumstances, plans and priorities, and your projection of what the future holds.

* The New York Times https://www.nytimes.com/2014/11/30/opinion/sunday/homeownership-and-wealth-creation.html

** National and multi-county San Francisco Metro Area house-price appreciation rates since 1990 per the S&P CoreLogic Case-Shiller Home Price Index, seasonally adjusted: https://my.spindices.com/index-family/sp-corelogic-case-shiller/sp-corelogic-case-shiller-composite. Inflation rate data from https://www.worlddata.info/america/usa/inflation-rates.php. Home prices can flatten or decline as well as increase, and different regions, market segments and property types have experienced wide variations in appreciation. Appreciation and inflation rates can fluctuate dramatically, even over the short term. Data from sources deemed reliable, but may contain errors and subject to revision. All numbers should be considered approximate.

Important: Consult a certified financial planner or accountant regarding tax-law and other financial issues pertinent to buying, owning, refinancing, renting or selling a home. Tax law is subject to change, and representations regarding tax law must be confirmed with a qualified professional as applicable to your specific circumstances. Renting out your home may affect the $250,000/$500,000 exclusion on capital gains taxes. Real estate agents are not qualified to advise on legal and tax matters. It is difficult to compare the costs of owning and renting, especially over an extended period that includes tax deductions, potential equity gain, inflation, and other cost and investment calculations. As with any investment, the exact timing of purchase and sale is a major consideration in the calculation of loss or gain, and real estate markets can be affected, positively and negatively, by a huge range of economic, political, demographic and environmental factors. Past performance is not a guarantee of future results.

Compass is a real estate broker licensed by the State of California, DRE 01527235.