Many experts will say you should not treat your home as an investment, but history shows that homes in Marin County have appreciated reliably over the decades.

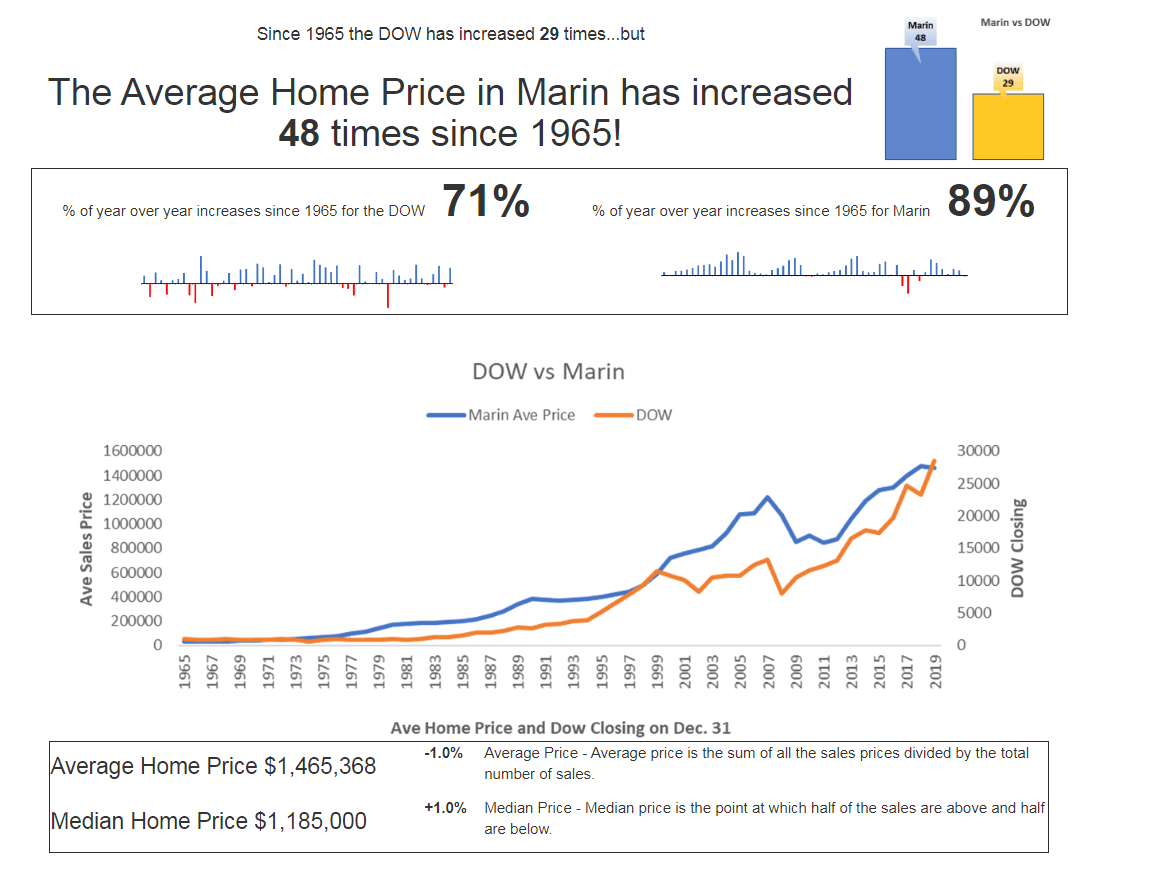

Below is a chart that shows the upward trajectory of home prices in Marin over the last 48 years and the comparison to the DOW. (Records go back to 1965.)

Below is a chart that shows the upward trajectory of home prices in Marin over the last 48 years and the comparison to the DOW. (Records go back to 1965.)

The main reasons to be bullish on home ownership for building wealth include return on investment and tax advantages:

- LEVERAGE: Leverage drives the impressive returns on investment (ROI) in homeownership. When a buyer purchases a home they are usually using OPM (Other People's Money), namely that of the bank or other lender. When the property appreciates in value, the appreciation is on the full price of the home; in other words, while the buyer may invest a 20% down payment in a home, they realize ROI on the full value.

For example, compare investing $300,000 in the stock market vs. in a down payment for a home that costs $1,500,000. When the value of the home appreciates, ROI is on the full price of the home compared to when the stock investment appreciates it's on the original investment. So a 10% increase in value on the home is $150,000 while a 10% increase in the stock investment is $30,000. And Marin real estate continues to trend up over time. (Assuming the buyer doesn't try to sell in too short a time period.) Of course, there are additional costs with home ownership but read on. - CAPITAL GAINS: The capital gains on the investment are exempt from taxes up to $500,000 in gains for married couples and $250,000 for single homeowners who have lived in the house as a primary residence for 2 of the preceding 5 years.* Gains in the stock market and other investments are generally not protected from taxes unless they are held in a retirement account. So on an investment made through a non-retirement account, if an investor makes $500,000 in the stock market they will owe capital gains taxes on the earnings.

- INTEREST DEDUCTION: The interest paid on the mortgage of a primary residence is deductible.* (Capped for mortgage amount. Consult your tax advisor for advice and details.)

- EQUITY BUILDING: Monthly payments build equity in the home over time. Rental payments are never recouped and offer no tax advantages.

- TANGIBLE ASSET: When there is a dip in the real estate market, homeowners don't lose everything in the way that wealth is wiped out when the stock market crashes; they still have the home, a tangible asset. And homes can be insured against loss, unlike most investments.

- HOME OFFICE TAX DEDUCTION: When homeowners work from home, there are additional tax advantages: the mortgage payments, insurance, home maintenance, office expenses, prorated utilities, etc. are tax-deductible for the portion used for the office space.* (Consult your tax advisor.)

*All tax law examples should be confirmed with your CPA or other tax law expert.

These are the financial advantages related to homeownership. The unquantifiable benefits of homeownership include:

- PRIDE OF OWNERSHIP: The desire to own your own home is a major part of the American Dream.

- SECURITY: The security from unexpected moves when the landlord decides to sell or raise the rent.

- QUALITY OF LIFE: The ability to design a home to one's taste including a possible remodel or expansion.

- UPGRADES: Equity builds in the home for an upgrade to a new house as life circumstances change.

- FORCED SAVINGS: Homeownership is a great way to sock away equity for future needs, especially retirement.

Share: